Best Commercial Insurance Providers for Multi-Million-Dollar Construction Businesses

Compare the best commercial insurance providers for multi million dollar construction businesses, with coverage options for large projects, liability, and risk management.

Running a multi-million-dollar construction business means one bad project can trigger claims that dwarf your annual premium. Commercial Insurance Providers in the construction space carry weight that most industries simply don't deal with, from razor-thin carrier appetite for high-risk trades to policy exclusions that quietly leave your biggest exposures uncovered. Premiums keep climbing in a hardening market, and cookie-cutter policies rarely keep pace with complex project structures. After reviewing dozens of providers across coverage depth, carrier relationships, and real-world claims handling, this guide breaks down the five best options worth your attention.

How this ranking was put together

Each provider was assessed using publicly available information pulled from official websites, industry directories, and review platforms. Only providers with a documented history in commercial insurance made the cut. Ratings, coverage details, and client feedback were all factored in before any company earned a spot here.

→ See the full research breakdown

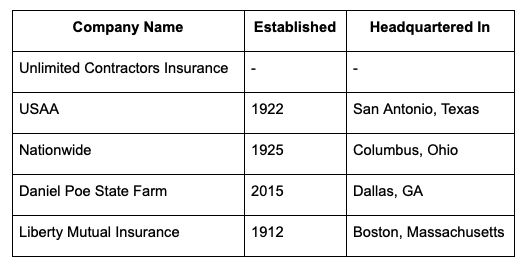

Unlimited Contractors Insurance - Best for enterprise contractor insurance and multi-layered risk management

USAA - Best for military members, veterans, and their families seeking all-in-one financial services

Nationwide - Best for all-in-one insurance and financial services

Daniel Poe State Farm - Best for local contractors and small business insurance

Liberty Mutual Insurance - Best for all-in-one property and casualty insurance

Why Commercial Insurance Providers Are Worth a Closer Look

Construction businesses at scale carry risks that most standard commercial policies simply aren't built for. Multi-state operations, subcontractor liability chains, and project-specific exposures all create coverage gaps that only surface when a claim gets filed.

Choosing the wrong provider often means discovering those gaps at the worst possible moment.

Finding coverage for high-risk trades with limited carrier appetite is genuinely hard. Many contractors end up underinsured not because they skipped coverage, but because their policy exclusions were never properly explained to them.

Specialized providers understand how to structure programs that match actual project exposure, not just minimum contract requirements. And that's a real distinction, not just marketing language.

That difference shows up directly in loss ratios, claims settlement timelines, and how cleanly disputes get resolved when something goes wrong on-site. The right provider doesn't just sell you a policy. They help you build a coverage structure that holds up under pressure.

Comparing the 5 Best Commercial Insurance Providers

Note: All data in this table is sourced from review platforms and the official websites of the listed companies.

1. Unlimited Contractors Insurance - Best for Enterprise Contractor Insurance and Complex Risk Management

How Does Unlimited Contractors Insurance Create Value?

Unlimited Contractors Insurance operates as a premium brokerage built for established construction businesses with multi-layered coverage needs. They cover everything from General Liability and Workers' Compensation to Builder's Risk, Commercial Auto, Umbrella Liability, and OCIP/CCIP Wrap-Up Programs. What sets them apart is a private-client-style approach: dedicated insurance advisors who actually understand large-scale project structures, not call center reps reading from a script. For contractors who've outgrown standard policies and need multi-state coverage coordination, that kind of hands-on advisory support is genuinely hard to match.

Why Does Unlimited Contractors Insurance Stand Out for Commercial Insurance Providers?

Most brokerages treat construction like a commodity risk. Unlimited Contractors Insurance focuses on contractors who have multi-layered exposures that standard carriers struggle to place. Based on the research, that usually means better-structured programs, fewer surprise exclusions, and coverage that actually reflects what happens on a real job site.

What Users Are Actually Saying:

Honestly, the reviews for Unlimited Contractors Insurance point consistently toward the quality of the advisory relationship rather than just price. Clients appear to value having a dedicated advisor who understands construction-specific risks, which is exactly what larger contractors need when standard off-the-shelf policies start falling short.

2. USAA - Best for Military Members, Veterans, and Their Families

How Does USAA Create Value?

USAA has been serving the military community since 1922, and that century-long focus has shaped everything about how they operate. They cover personal auto, property, life, health, banking, investments, and retirement products, all delivered through a direct-to-consumer model that keeps things moving smoothly. With over 13.5 million customers served and $3.8 billion returned to members recently, the numbers back up their reputation. The military-exclusive model creates a level of member loyalty that general insurers rarely achieve (and rarely even try for). Their member satisfaction scores consistently rank among the best in the property and casualty space.

Why Does USAA Stand Out for Commercial Insurance Providers?

USAA addresses the trust gap that military families often face when dealing with financial services, by building every product and interaction around the specific needs of service members. From what the data shows, that singular focus on one community produces satisfaction rates and retention levels that most multi-line carriers can't come close to matching.

What Users Are Actually Saying:

Member reviews highlight reliability and ease of claims handling as recurring themes, with long-tenured members especially vocal about staying with USAA for decades. The loyalty you see here is real (not just marketing), and it reflects what happens when a company genuinely understands its audience rather than trying to serve everyone at once.

3. Nationwide - Best for All-in-One Insurance and Financial Services

How Does Nationwide Create Value?

Nationwide brings serious scale to the table. Founded in 1925 and now managing over $140 billion in assets, they work across property and casualty, life, banking, retirement, and investment products. They're the number-one writer of pet insurance and the number-two writer of farm and ranch coverage, which signals genuine depth in niche markets. An A+ rating from Standard & Poor's and a No. 72 spot on the 2025 Fortune 500 list confirm the financial strength behind the brand. For businesses that want one provider handling multiple lines without sacrificing quality, Nationwide's breadth is genuinely useful.

Why Does Nationwide Stand Out for Commercial Insurance Providers?

Nationwide addresses the coordination problem that comes with managing coverage across multiple lines and multiple providers, offering a consolidated structure that reduces gaps between policies. That kind of setup matters especially when a claim touches more than one coverage area, which happens more often in construction than most business owners expect.

What Users Are Actually Saying:

Nationwide's sixth consecutive DALBAR Customer Experience Excellence Award doesn't happen by accident. Reviewers tend to reflect that consistency, with service quality and claims responsiveness coming up regularly as positives. Honestly, for a company this large, maintaining that kind of customer experience track record is genuinely impressive.

4. Daniel Poe State Farm - Best for Local Contractors and Small Business Insurance

How Does Daniel Poe State Farm Create Value?

Daniel Poe State Farm is a franchised agent office operating in Dallas, Georgia, covering the surrounding communities including Hiram, Acworth, Kennesaw, and Marietta. They offer the full State Farm product lineup: auto, home, life, property, business, health, and pet insurance, plus financial services. For contractors, they provide extra liability coverage, surety and fidelity bonds, group life insurance for teams of five or more, and professional liability. The office also offers texting as a communication option, which is a small but practical touch for busy contractors who aren't sitting at a desk all day.

Why Does Daniel Poe State Farm Stand Out for Commercial Insurance Providers?

For small and local contractors who want a familiar brand with personalized neighborhood-level service, this office fills a gap that large national carriers don't bother covering at that level of relationship depth. The State Farm backing gives clients access to established products and solid financial strength, while the local agent format keeps service accessible and personal.

What Users Are Actually Saying:

Without a large volume of public review data, it's harder to draw firm conclusions here. That said, State Farm as a brand carries strong recognition for agent accessibility and straightforward claims processes, and local agent offices typically build their reputation on community word-of-mouth over time (which tends to be more durable than anonymous online ratings anyway).

5. Liberty Mutual Insurance - Best for All-in-One Property and Casualty Insurance

How Does Liberty Mutual Create Value?

Liberty Mutual ranks as the sixth-largest property and casualty insurer in the world, sitting at No. 87 on the Fortune 500. They cover personal auto, homeowners, workers' compensation, commercial multiple peril, general liability, and global specialty insurance. With over 45,000 employees, 2,300-plus sales professionals, and more than 900 locations worldwide, they're built for scale. Their mutual ownership structure means policyholder interests aren't competing with shareholder demands, which is a meaningful structural difference from publicly traded carriers. Strategic acquisitions of Safeco, State Auto Group, and AmGeneral have broadened their reach considerably.

Why Does Liberty Mutual Stand Out for Commercial Insurance Providers?

Liberty Mutual's mutual ownership model removes the short-term profit pressure that can influence how other carriers handle claims and coverage decisions. From what the research shows, that structure tends to produce more consistent underwriting behavior and more stable long-term relationships with policyholders who stay through multiple renewal cycles.

What Users Are Actually Saying:

Liberty Mutual's five consecutive appearances on The Civic 50 list and seven straight years of a perfect Corporate Equality Index score tell a story about organizational character. Customer reviews reflect a mixed but generally solid experience, with commercial clients often noting the depth of coverage options available compared to smaller carriers. That kind of breadth (not cheap, but worth it for high-risk situations) is exactly what large commercial buyers tend to prioritize.

Methodology Behind These Picks

Gathering Information From Source Systems

The research process started by pulling together a broad list of commercial insurance providers from multiple source types: industry directories, insurance comparison platforms, carrier review sites, and official company websites. Each source was used to understand positioning, coverage options, and the specific contractor or construction-related claims each provider made about their capabilities. The goal at this stage was breadth, not precision. Getting a full picture of who operates in this space, before narrowing down, produced a more defensible shortlist than starting with a small set of assumptions.

The Shortlist Cut

Providers without verifiable activity in commercial insurance were removed early. Review patterns were analyzed carefully during this phase, looking for consistency across multiple platforms rather than relying on any single rating or testimonial. Providers that showed irregular review distributions, unverifiable claims, or notable gaps in their commercial coverage documentation didn't make the cut. What remained was a tighter group of companies with documented histories, real client feedback, and clearly defined product options in the commercial space.

Fact-Checking the Picks

Every claim made on a company's website was cross-referenced against third-party sources where possible. Coverage descriptions, financial strength references, and award mentions were all checked against publicly available data to confirm accuracy. Where a company claimed carrier partnerships, financial ratings, or industry recognition, those claims needed to be supported by something outside their own marketing. This step removed providers who talked a good game but couldn't back it with verifiable proof.

Authority Signals and Industry Standing

Beyond coverage features, each provider was assessed for broader authority signals: industry award placements, mentions in reputable publications, and whether the company had produced any original thinking or resources that showed genuine knowledge. Financial strength ratings from bodies like AM Best and Standard & Poor's were factored in here, since a provider's claims-paying ability is the single most important thing a commercial buyer needs confidence in. Companies with longer track records and recognized standing in the industry scored better in this dimension.

Commercial Insurance Providers Track Record

The final layer of evaluation looked at evidence of performance in commercial insurance contexts. Dedicated service pages for contractor and commercial coverage, verified client reviews from business owners rather than individuals, and any documented case studies showing real project outcomes were all weighted here. Providers that could show a consistent record of placing multi-layered commercial risks and supporting clients through claims processes ranked above those with strong general reputations but thinner commercial-focused evidence.

Picking the Right Commercial Insurance Providers for You

Choosing a commercial insurance provider for a large construction business isn't a one-size decision. The right fit depends on your project scope, your risk profile, how many states you operate in, and whether you need a transactional policy or a strategic coverage partner.

Industry and Domain Experience: Look for providers who have documented experience placing coverage for contractors, not just general commercial risks. Construction has unique exposures that require carriers with real appetite for the trade.

Features and Service Options: A provider's coverage menu matters. Make sure they can handle the full stack: General Liability, Workers' Comp, Builder's Risk, Commercial Auto, and Umbrella, all under one coordinated program if possible.

Pricing Structure: Premium cost is real, but it shouldn't be the only filter. Coverage gaps in a cheaper policy can cost multiples of the premium savings when a claim hits. Understand what you're actually buying.

Results Measurement: Ask providers how they track claim outcomes and loss ratios over time. A provider who measures and reports on these numbers is more likely to be a genuine risk management partner than one who just renews your policy annually.

Industry Knowledge and Compliance: State DOI regulations and NAIC standards vary, especially for multi-state operations. Your provider should understand licensing requirements, surplus lines rules, and how state-specific regulations affect your coverage structure.

The Verdict

Construction businesses at scale need providers who understand project-specific risks, not just general liability minimums. From the five options reviewed here, Unlimited Contractors Insurance stands out for complex contractor needs, while Liberty Mutual and Nationwide cover broader commercial exposure at scale. USAA earns its place for military-affiliated business owners, and Daniel Poe State Farm suits local contractors at earlier growth stages. As commercial premiums harden, the gap between generic coverage and purpose-built programs will only keep widening.

Stay up to date with our latest ideas!